| IMF blueprint for a global currency ñ yes really Financial

Times | August 4, 2010

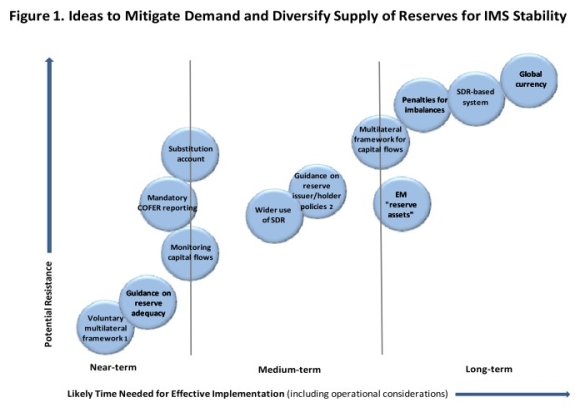

FT Alphaville missed this IMF paper when it first came out in April, 2010. Authored by Reza Moghadam, director of the IMFís strategy, policy and review department, it discusses how the IMF sees the International Monetary System evolving after the financial crisis. Weíll cut to the chase and draw readersí attention to the final bubble in the following chart, found on page 4: |

| Which means, in the eyes of the IMF at least, the best way to ensure

the stability of the international monetary system (post crisis) is actually

by launching a global currency.

And that, the IMF says, is largely because sovereigns ó as they stand ó cannot be trusted to redistribute surplus reserves, or battle their deficits, themselves. The ongoing buildup of such imbalances, meanwhile, only makes the system increasingly vulnerable to shocks. Itís also a process thatís ultimately unsustainable for all, says the IMF. Or as they put it: The global crisis of 2008/09, for all its costs, has not jeopardized international monetary stability, and the IMS is not on the verge of collapse. That said, the current system has serious imperfections that feed and facilitate policiesóof reserves accumulation and reserves creationóthat are ultimately unsustainable and, until they are reversed, expose the system to risks and shocks that a reformed system could minimize.All in all, the IMF believes there has simply been too much reserve hoarding going on: Reserve accumulation has accelerated dramatically in the past decade, particularly since the 2003-4. At the end of 2009, reserves had risen to 13 percent of global GDP, doubling from their 2000 level, and over 50 percent of total imports of goods and services. Emerging market holdings rose to 32 percent of their GDP (26 percent excluding China). Twenty-seven of the top 40 reserve holders, accounting for over 90 percent of total reserve holdings, recorded doubledigit average growth in reserves over 1999-2008.Of course, in the first instance, the solution probably lies in closer collaboration between sovereigns, most likely via the more active use of such things as special drawing rights, says the IMF. But in the end, a global currency makes the most sense, the paper concludes ó especially since the SDR is currently just an accounting tool that draws on the freely usable currencies of member states , not an actual currency itself. As they summarise: 48. From SDR to bancor. A limitation of the SDR as discussed previously is that it is not a currency. Both the SDR and SDR-denominated instruments need to be converted eventually to a national currency for most payments or interventions in foreign exchange markets, which adds to cumbersome use in transactions.But before you get ready to burn your fiat currency, itís not actually a turnaround the IMF sees being executed any time soon. As they conclude: It is understood that some of the ideas discussed are unlikely to materialize in the foreseeable future absent a dramatic shift in appetite for international cooperation. |